— September 20, 2018

Can businesses that still pull in revenue go bankrupt?

The answer is yes.

So how can small business owners prevent this from happening to them?

From discounted cash flow analysis to cash flow projections, there are a number of methods to help business owners properly manage cash flows. After all, managing your cash flows is key to a successful business.

Data from a recent study analyzing 101 startups found that 29 percent of businesses failed because they ran out of money. CB Insights, the organization that conducted the study, found running out of money was the second top reason startups fail.

By looking at your current cash flows and making projections or forecasts, you’ll be better equipped to handle potential financial issues. This is one of the most essential methods for protecting your business.

How Can a Cash Flow Forecast Help?

When you conduct a cash flow forecast, you’re looking at how much money you currently have on hand and estimating your business’s revenue and expenses in the future. By doing this, you can get a better idea of your business’s financial standing and give yourself a better opportunity to address any financial issues early on.

If your business has been steadily growing and you’re looking to invest in some equipment or another asset, conducting a cash flow forecast can help you figure out if you have enough money to fund it. Depending on your financial situation, a forecast can help you determine if you need to consolidate to save money in the future or if you can afford an expansion to continue business growth.

A cash flow forecast can also tell you if you have enough cash to complete customer orders and pay your employees in the future. If you identify a shortfall down the road, the forecast gives you the opportunity early on to make changes.

Types of Cash Flow Forecasts

There are three different ways to conduct a cash flow forecast: short term, medium term, and long term.

Figuring out which cash flow forecast to conduct depends on your goals and your business’s financial standing.

- Short-term cash flow forecast: A short-term cash flow forecast usually covers a period of two to six months and it looks at cash flows every day. You’ll use a short-term forecast when you have an immediate need to know how much money you have on hand and any upcoming bills and expenses. A short-term cash flow forecast can help you identify a period where you may not have enough money for something and allows you to address it immediately. If a short-term cash flow forecast shows you’ll have a surplus down the road, you may be able to put it into an investment account to grow your business.

- Medium-term cash flow forecast: A medium-term cash flow forecast looks at a year’s worth of information. A medium-term cash flow forecast can typically tell you how much money you’ll need at certain points of the year for expenses, as well as any cash surpluses you may be able to expect within the next year. This type of cash flow forecast can be particularly helpful for seasonal businesses to ensure there is enough money to get them through the quiet season of their business.

- Long-term cash flow forecast: A long-term cash flow forecast covers more than one year. This kind of cash flow forecast includes longer-term purchases and projects. Because a forecast is based on assumptions, the data becomes less reliable and it becomes more difficult to predict performance.

How Do You Conduct A Cash Flow Forecast?

Before you actually conduct a forecast, you’ll need to make sure you have some information and data beforehand.

You should have a realistic estimation of revenue and expenses for the time period you’re looking at. It’s important you don’t get too optimistic with your data. If you do, you run the risk of having an inaccurate forecast.

One way to try to get the most accurate estimations is to look at your business’s performance in the past. You’ll see sales trends and any spending patterns throughout the year. Bank statements will also show you what your business spent money on. Don’t forget about other streams of income and expenses that can come up throughout the year. Tax refunds or credits should be accounted for, as well as paying for taxes and insurance policies.

Once you have the information you need, you can conduct a cash flow forecast. Here’s what you’ll do:

- For each time period, you’ll list out the income and expenses.

- Add the income and any cash you currently have on hand. Add up the expenses.

- Subtract the total income by the total expenses. This will give you estimated net revenue for that specific time period.

Here’s a formula you can use to help:

(Cash on hand in the time period + Total Income) – Total Expenses = Net Revenue for the time period

Here’s a quick example. Let’s say you’re conducting a medium-term forecast for the upcoming year that looks at cash flows on a month-to-month basis. You have $ 8,000 on hand and are projected to make $ 25,000 next month. You’re also estimated to spend $ 19,000. Using the formula above, you can find the projected net revenue for the month:

Repeat these steps for the rest of your forecast and you’ll be able to see where you’ll have any cash shortfalls or surpluses in the year.

Can You Conduct A Cash Flow Forecast In Excel?

Conducting a cash flow forecast in Excel is a great way to organize all of this information. So how do you properly set up the spreadsheet? Here’s how:

- First set up the A column:

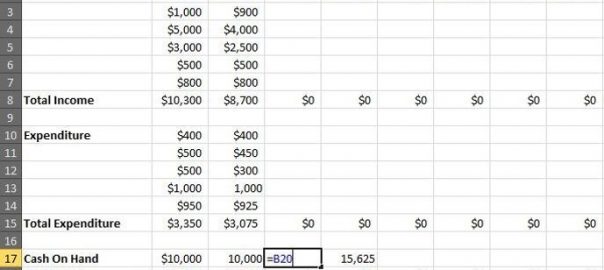

-

- In the first cell in the A column, label it “Income.” A few cells down in the same column, put “Total Income.”

- Go down another two cells and label it “Expenditure.” Leave a few cells blank and then label another cell “Total Expenditures.”

- Go down an additional two cells and put “Cash On Hand.” Underneath that, put “Add Total Income,” “Less Total Expenditure,” and “Cash Leftover” in its own cells.

- You’ll now set up the time in the forecast. In this example, a month-to-month forecast is being set up.

- In the first cell of column B, put the month that follows the one you’re currently in. Leave the adjacent cell (in column C) empty. Repeat the process in column D and the other columns until you’ve put in every month you’re looking at.

- Highlight one month and the blank cell next to it. Click the Merge function in the “Alignment” section, which looks like the letter A in between two arrows. This will make it easier to read and put in new data for your forecast. Repeat this process for each month.

- Under each month, add “Forecast” and “Actual” in the cells in the columns B and C.

- Fill in the forecasted income for the month. To calculate the “Total Income,” click on the cell and use the “sum” function, which is the S symbol in the “Editing” section of the toolbar. Click on the cell and drag the bottom right corner out across your spreadsheet. This will tell Excel to use the same sum function for each month.

- Fill in the forecasted expenditures for the same month. Click on the same S symbol to calculate the total forecasted expenditures. Click on the cell and drag the bottom right corner out across the spreadsheet.

- In the cell for “Cash On Hand,” put the amount of money you have on hand. This will be the same number for the actual column in the first month.

- In the “Add Total Income” cell, put “=(cell number for “Total Income”). In this case, it would be “=b8.” Click on the cell and drag the bottom right corner out across the spreadsheet.

- Do the same for the “Less Total Expenditure,” but be sure to put in the correct cell number for the total expenditure.

- In the cell next to “Cash Leftover” put “=(cell number for “Cash On Hand”)+(cell number for “Add Total Income”)-(cell for “Less Total Expenditure”). Click on the cell and drag the bottom right corner across the spreadsheet.

- In column C, the “Cash On Hand” is going to be the number in the “Cash Leftover” cell in the forecasted column. In this case, it’ll be the number in cell B20. Click on the cell in column D and put “=B20.”

- You can do the same thing for the “Actual” figures. The “Cash On Hand” figure in the Actual column for the next month will be the previous month’s Actual “Cash Leftover.”

Updating Your Forecast Regularly

After you’ve set up your spreadsheet and figured out the forecasted cash flows for your business, it’s equally important to go back into your spreadsheet and update it with the figures for actual income and expenditures.

This is a good way to see if your assumptions were realistic or if they were overly optimistic. It will also help you in the future if you decide to conduct another cash flow forecast.

So how often should you update your forecast? Any time something happens with your business, you should update your spreadsheet. If a customer pays you for an order, you should go into your forecast and add that into the correct time period as income. Likewise, if you spend money on something, that should be reflected in the respective time period in your forecast.

Regularly checking your forecast gives you an opportunity to make sure you’re working with an accurate number for your current cash flow. You can think of it as balancing your business’s checkbook; you want to make sure the forecast’s numbers have the most up-to-date income and expenses reflected in it.

Cash Flow Forecasts: Helping You Manage Your Business’s Money

Properly managing your business’s money is vital to making sure your company not only survives but succeeds. A cash flow forecast can help you figure out how much money you currently have on hand and how much money you’ll have in the future.

Conducting a cash flow forecast can also help you identify any cash shortfalls you may run into in the future. The benefit to this is you’ll identify the issue early on.

Although putting together a cash flow forecast can take time, it’s an important tool for business owners.

Business & Finance Articles on Business 2 Community

(107)

Report Post