Introduction

Since the Great Recession of 2008 came to an end, the stock market, as measured by the S&P 500, is almost midway through the 7th year of a strong bull run. This marks today’s bull market as the third longest in US history. Considering how traumatizing the Great Recession and the accompanying stock market collapse was for most investors, this should be good and comforting news. But unfortunately, the length and level of our current bull market seems to be conjuring up more worry and angst than comfort.

For some time now, many investors have been lamenting that stocks have become too expensive, and some are even playing the bubble card. However, prudent investing requires separating fact from fiction. Therefore, prudence would also dictate taking a more analytical and less emotional evaluation of the true state and level of today’s stock market. Have stocks truly become too expensive to invest in, more to the point, have all stocks become too expensive in lockstep with the market? Perhaps recent market history and precedents will provide answers.

May 2015: A Fundamental Valuation Analysis of the S&P 500

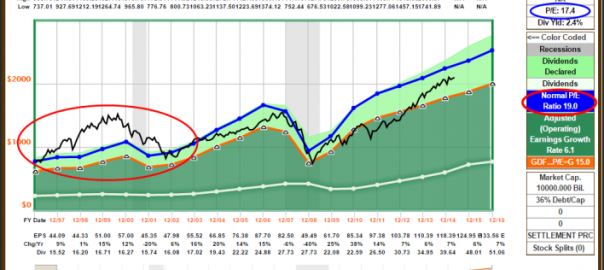

Utilizing the analytical power of the F.A.S.T. Graphs™ fundamentals analyzer software tool, let’s take a factual look at the S&P 500’s typical valuation ranges over recent history. The current blended P/E ratio of the S&P 500 sits between 17 and 18 times earnings. If we review the historical normal P/E ratio of approximately 19 for the market since 1997, the argument could be made that the general market might be modestly undervalued. However, that timeframe includes the high P/E ratios that the market traded at during the irrational exuberant period of the mid-1990’s to 2000 that skewed the average P/E ratio calculations upwards.

Consequently, if we only include the timeframe 2002 to current, we discover perhaps a more appropriate historical normal P/E ratio of 17. On that basis, the argument could be made that the market, as measured by the S&P 500, is currently being valued at historically normal levels. This would indicate that the market is not necessarily cheap, nor is it significantly overvalued. Instead, it might be rational to conclude that the market is currently fully valued. In other words, the S&P 500 is currently not a bargain, but nor is it dangerously overvalued, at least based on recent historical precedent.

But most importantly of all, the above analysis supporting a fully-valued market in the general sense does not necessarily mean that all stocks are fully valued or even priced high if that is your view. Nevertheless, the above analysis does support the reality that with the market levels where they are today, it has become exceedingly more difficult to find sound investment opportunities or good bargains to invest in. This is a challenge for investors that currently have money that needs to be invested. The good news is that there are still good and sound long-term investment opportunities available if you’re willing to look beyond generalities such as – the stock market is too high.

For loyal Seeking Alpha readers I offer this link to a past article that contains a live fully functioning F.A.S.T. Graphs™ on the S&P 500 that can be utilized to analyze the current state and valuation of the market.

Johnson Controls Is Not an Overvalued Stock

Prudent long-term dividend growth or retired investors should not let market hype scare them away from this excellent long-term total return and above-average dividend growth investment opportunity. Although this company is not on the radar screens of many conservative long-term investors, I believe it has great long-term appeal. Johnson Controls (JCI) has paid a dividend every year since 1887 and increased its revenues for 62 consecutive years until the Great Recession. However, the interruption in growth was short-lived and the company is back on its typical growth track as I will soon illustrate.

Johnson Controls Essential Fundamentals at a Glance

Johnson Controls is an attractively valued high quality dividend growth stock possessing long-term appeal for potentially generating an above-average total return and dividend growth. However, before digging deeper into the opportunity that Johnson Controls offers today, let’s start by taking a historical look at the company’s essential fundamentals at a glance through the fundamental analytical power of F.A.S.T. Graphs™. The primary objective of this exercise is to establish a perspective of how well this company has performed as an operating business, coupled with how the market has typically treated that performance.

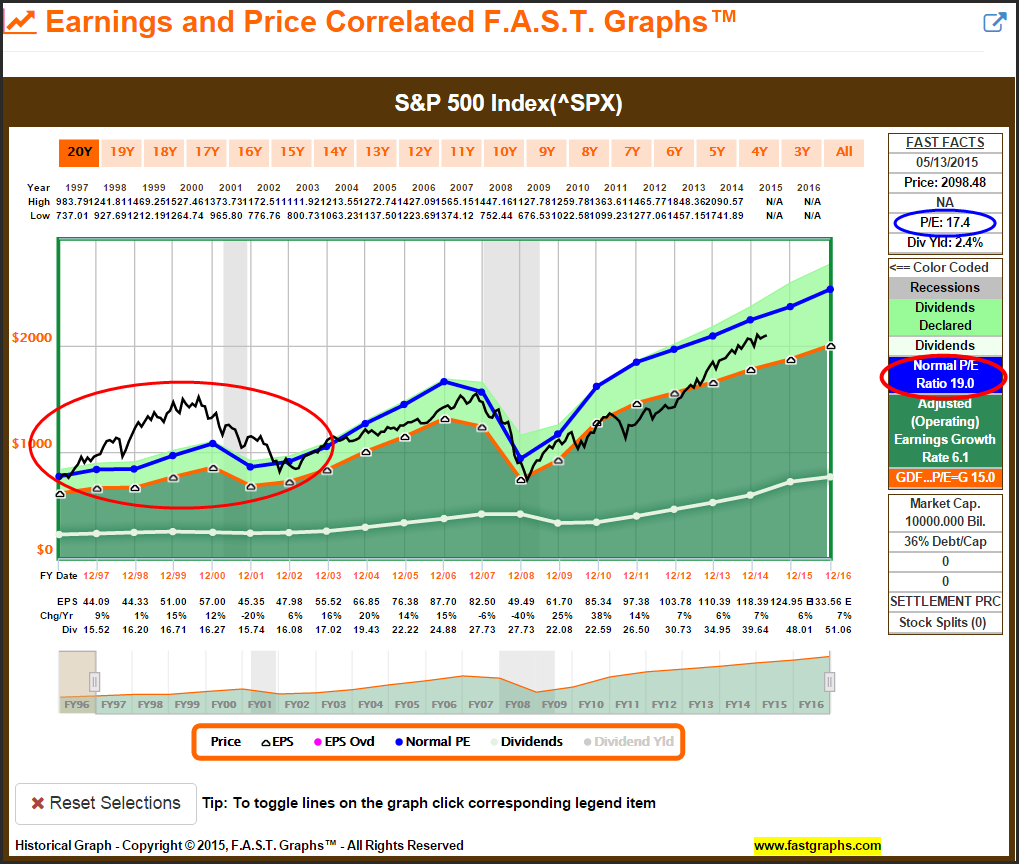

In order to establish the clearest perspective, I will start out by presenting the essential fundamentals of earnings and dividends without the emotional contamination that stock prices bring to the equation. Additionally, I will first look at Johnson Controls over the timeframe 1996-2007 in order to analyze its operating results prior to the Great Recession. From there I will update to current time and review operating results during and after the Great Recession.

From 1996-2007 Johnson Controls generated an almost flawless operating record based on earnings and dividend growth. Earnings grew from $ .48 at fiscal year-end 1996 to $ 2.33 by fiscal year-end 2007 representing a compound annual growth rate of 15.2%. In concert, Johnson Controls’ dividend grew from $ .14 to $ .52 for a compound annual growth rate of 10.7%.

To get my complete research regarding Johnson Controls free of charge, visit misterVALUATION and pre-register for the launch of my new site. There I will provide more in-depth analyses on all of my research recommendations, to include a FAST Graph video analysis as I evaluate the research candidate on a live FAST Graph. All you need is a valid email address, with no obligation.

When monthly closing stock prices are added to the graph, we discover a strong correlation between price (the black line) and earnings (the orange line). Clearly, price followed earnings and periods of undervaluation (price below the orange line) and overvaluation (price above the orange line) are visibly revealed. Most importantly, the graph clearly illustrates that periods of overvaluation and undervaluation were short-lived as price inevitably, and reasonably quickly, returned to alignment with fair value (the orange line). Consequently, we are given a distinctive perspective of optimum and sound buying opportunities.

A quick review of the return performance over this timeframe compared to the S&P 500 illustrates that prior to the Great Recession Johnson Controls was an excellent long-term investment. Both dividend income and capital appreciation significantly outpaced the S&P 500.

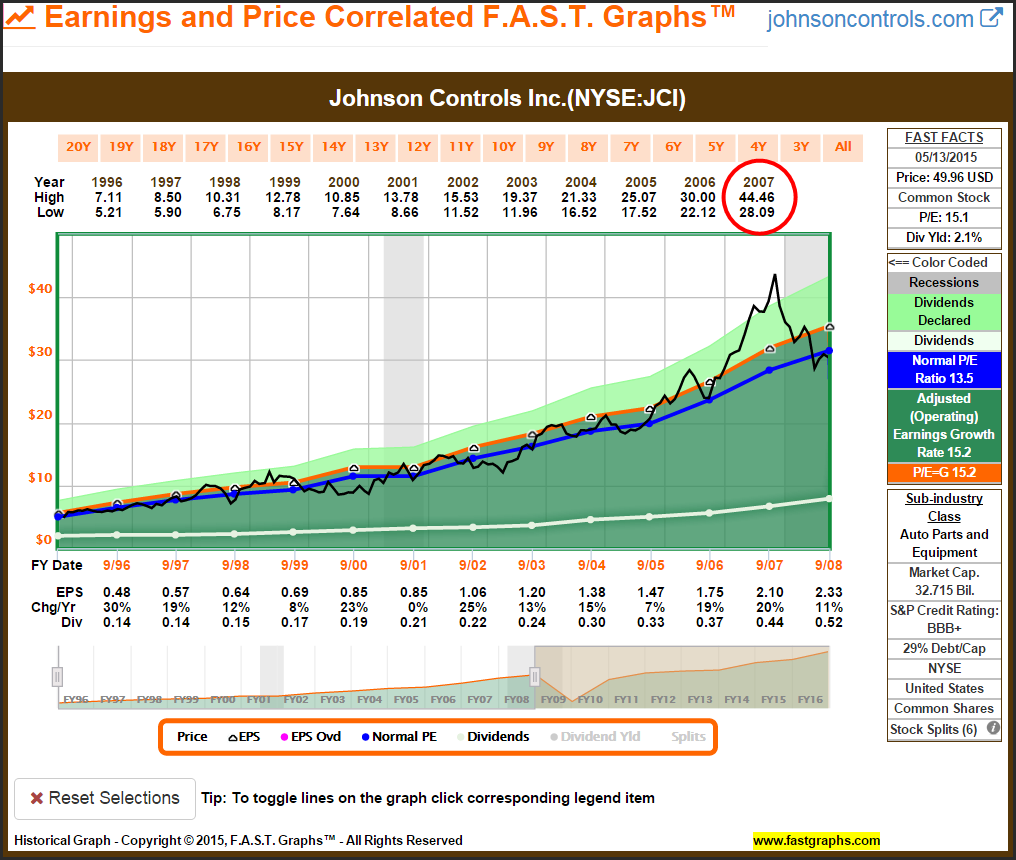

However, as I will cover in more detail later, the Great Recession not only took its toll on the company’s earnings record, it also revealed a significant vulnerability. The company’s strong exposure at that time to the cyclical North American automotive industry led to an earnings collapse of approximately 80% for fiscal year end 2009, virtually wiping out years of impeccable and consistent growth. It’s important to note that the company did remain profitable, but just barely.

Fortunately for shareholders, Johnson Controls’ cash flows held up better than earnings, allowing management to continue paying a dividend at the 2008 rate. However, the dividend was frozen through fiscal year 2010, but has since been growing again at their historically normal rate. Importantly, the following graph also shows that earnings recovered quickly and exceeded historical highs by fiscal year-end 2010, and Johnson Controls’ stock price responded accordingly. As I will also discuss later, a lot has changed and improved with Johnson Controls since the Great Recession debacle, and earnings, dividends and price are back on their historical track of growth and excellence.

The final reveal that this exercise provides is that Johnson Controls is currently available for investment at fair or sound value. Therefore, this provides evidence that a deeper look and a more comprehensive research effort on Johnson Controls is justified and warranted.

Reasons Why I Favor Johnson Controls

Short Business Description Courtesy S&P Capital IQ:

“Johnson Controls, Inc. operates as a diversified technology and industrial company worldwide.

Its Building Efficiency segment designs, produces, markets, and installs integrated heating, ventilating, and air conditioning systems, as well as building management systems, controls, and security and mechanical equipment. This segment also provides technical services, energy management consulting, and operations of real estate portfolios for the non-residential buildings market. In addition, this segment offers residential air conditioning and heating systems, and industrial refrigeration products.

The company’s Automotive Experience segment designs and manufactures interior products and systems for passenger cars and light trucks, including vans, pick-up trucks, and sport/crossover utility vehicles serving original equipment manufacturers. This segment offers automotive seat metal structures and mechanisms, foam, trim, fabric, and seat systems; and instrument panels, floor consoles, and door panels, as well as cockpits.

The company’s Power Solutions segment produces lead-acid automotive batteries for passenger car, light truck, and utility vehicles, as well as offers advanced battery technologies to power Start-Stop, hybrid, and electric vehicles. It serves automotive original equipment manufacturers and the general vehicle battery aftermarket.

The company was formerly known as Johnson Electric Service Company and changed its name to Johnson Controls, Inc. in 1974. Johnson Controls, Inc. was founded in 1885 and is headquartered in Milwaukee, Wisconsin.”

Johnson Controls Transforming Itself into High-Margin Growth Businesses

Since the Great Recession of 2008, Johnson Controls has significantly diversified and rebalanced their business which has offset their once lopsided exposure to the extremely cyclical North American automotive industry. In 2014 their combined exposure to the automotive sector decreased to approximately 50% from approximately 70% prior to the Great Recession. As a result, the company is now less vulnerable to future recessions.

MorningStar had this to say about Johnson Controls’ transformation initiatives:

“Johnson Controls has been engaged in a multi-year transformation involving the divestiture of its lower margin businesses and acquiring higher margin businesses that will increase its profitability in the intermediate and long term. In recent quarters, the company struggled with consistent revenue growth, even though the company had shown operational improvements across all of its businesses. Given JCI’s lack of consistent revenues and earnings growth, the company’s earnings growth is below the earnings growth of its competitors, and, therefore, the market is assigning a price-to-earnings multiple to JCI that is lower than the price-to-earnings ratio assigned to its competitors.

In recent weeks, the company announced its largest and likely its last few major transactions in the intermediate term. First, JCI announced an agreement for the sale of its Global WorkPlace Solutions (“GWS”) business to CBRE Group, Inc. for $ 1.475 billion.

Second, JCI and Yanfeng Automotive Trim Systems Co., Ltd. announced an agreement for a global automotive interiors joint venture, whereby Yanfeng will hold the majority 70 percent share in the joint venture, and Johnson Controls will hold a 30 percent share. Each of these transactions, the company’s most significant transformational actions to date, allow JCI to unload significant portions of its low margin businesses.

JCI expects fiscal year 2015 results to be better than fiscal 2014 results given higher profitability in all three of its businesses due to the company’s strategic and financial plans leading to better performance and higher operating margins.

JCI exited two relatively small, capital intensive businesses to enter a business that has margins nearly double its overall net margin. In mid-2014, JCI announced its plan to spin off its low-margin, slow-growth auto interiors business into a joint venture with a division of the Chinese company SAIC. In recent weeks, however, JCI announced its most significant transactions to date that support its effort to transform the company towards higher margin businesses.

Each of the company’s divestitures or acquisitions will allow it to exit low-margin businesses and enter higher margin businesses. With the company’s transformational transactions nearing completion, the major components of the company’s strategy are largely complete. The results from the company’s transactions will become more appreciated by investors in the intermediate term. Near term, however, many investors are failing to appreciate the effect the company’s divestitures and acquisitions will have on the company’s profitability in the intermediate and long term. Further, JCI’s transformation will allow it to capitalize on future trends, such as the energy efficiency concerns of office tower owners and energy efficient battery technology.”

Today the company’s three primary businesses, the Automotive Group, Building Efficiency and Power Solutions, are all promising and highly profitable growth opportunities.

The Automotive Experience is a $ 22 billion segment:

The automotive group currently has excellent growth potential as the company is investing heavily in China, the world’s largest automotive market. However, the North American and European markets remain strong and large contributors to this segment.

Building Efficiency is a $ 14.2 billion segment:

The building efficiency segment is currently experiencing a surge in demand as orders were up strongly, and their backlog strong at over 4 ½ billion dollars. This segment also showed strong margin improvement in the second quarter of 2015.

Power Solutions is a $ 6.6 segment:

Their power solutions segment (high-tech batteries) is showing strong growth throughout the world. Margins are also improving thanks to higher volumes and a better mix of higher-margin products. Johnson Controls is the undisputed leader in AGM (absorbent glass mat) batteries making them the major provider of the rapidly growing trend in vehicle “Start – Stop” technology serving automotive manufacturers’ growing need to produce more fuel-efficient vehicles.

Johnson Controls Ethical, Competent, and Shareholder Friendly Management

In addition to Johnson Controls’ excellent operating legacy, their management is also highly regarded as one of the most ethical and shareholder friendly. The following taken directly from their website highlight some of their most recent acknowledgments:

AWARDS AND RECOGNITION

Johnson Controls is honored to be recognized by our customers, our suppliers, our communities and others for the value and service we provide.

Leadership

- One of Corporate Responsibility magazine’s “Best Corporate Citizens”

- One of Ethisphere magazine’s “World’s Most Ethical Companies”

- One of Fortune magazine’s “America’s Most Admired Companies” in the “motor vehicle parts” category

- 2013 All-American Executive Team, Institutional Investor magazine

Diversity

- For the 10th consecutive year, Johnson Controls earned a seat at the Billion Dollar Roundtable, a select group of 18 companies that spend more than $ 1 billion annually with diverse suppliers

- 2013 Corporation of the Year, Michigan Minority Supplier Development Council

- 2013 Superior Award for Supplier Diversity Initiatives from Toyota North America

- DiversityInc. 25 Noteworthy Company 2013

- China Top Employer 2012 & 2013

- 2014 GI Jobs Top Military Friendly Employers

Johnson Controls’ management team has also long been recognized for its shareholder friendly approach to running its business. In addition to its long-standing dividend record cited above, the Board of Directors and executive committee have a well-documented commitment to a shareholder friendly compensation plan as evidenced by the following documentation.

Johnson Controls’ executive compensation objectives and philosophy:

MorningStar research summarized Johnson Controls’ executive compensation succinctly as follows:

“We like that senior management is compensated based on shareholder-friendly metrics such as pretax return on equity and pretax return on invested capital instead of more short-term measures, such as earnings per share.”

Johnson Controls, Inc. 5757 North Green Bay Ave. Milwaukee, Wisconsin 53209-4408

Notice of 2015 Annual Meeting and Proxy Statement

Worldwide Presence and Leadership

Johnson Controls is a global diversified technology and industrial leader serving customers in more than 150 countries.

Johnson Controls’ Total Return Opportunity

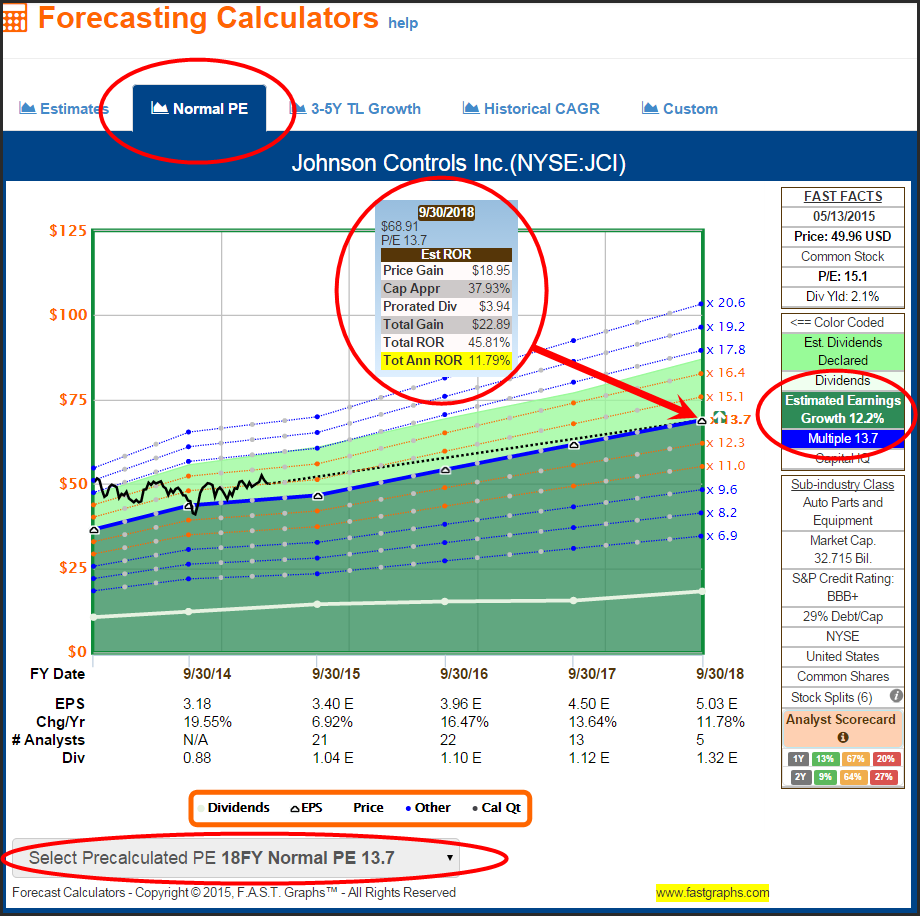

As described above, Johnson Controls appears to have righted the ship and transformed the company as a result of the lessons learned from the Great Recession. Since fiscal year-end 2010 the company has achieved an average operating earnings growth rate better than 12% per annum. Consequently, the consensus forecast earnings growth rate of 12.2% by leading analysts following the company seems reasonable and achievable. If that is true, then the following forecasting calculator illustrates the potential to earn approximately 15% per annum over the next 2 to 3 years. That’s a solid potential rate of return, especially considering what might be available from the market or most other equal quality companies.

If we then turn to the forecasting calculator based on the long-term normal P/E ratio suggesting a minor P/E ratio contraction to 13.7, we still see an opportunity for double-digit rates of annualized total returns. Since I consider this a conservative case, I’m quite pleased with the calculation.

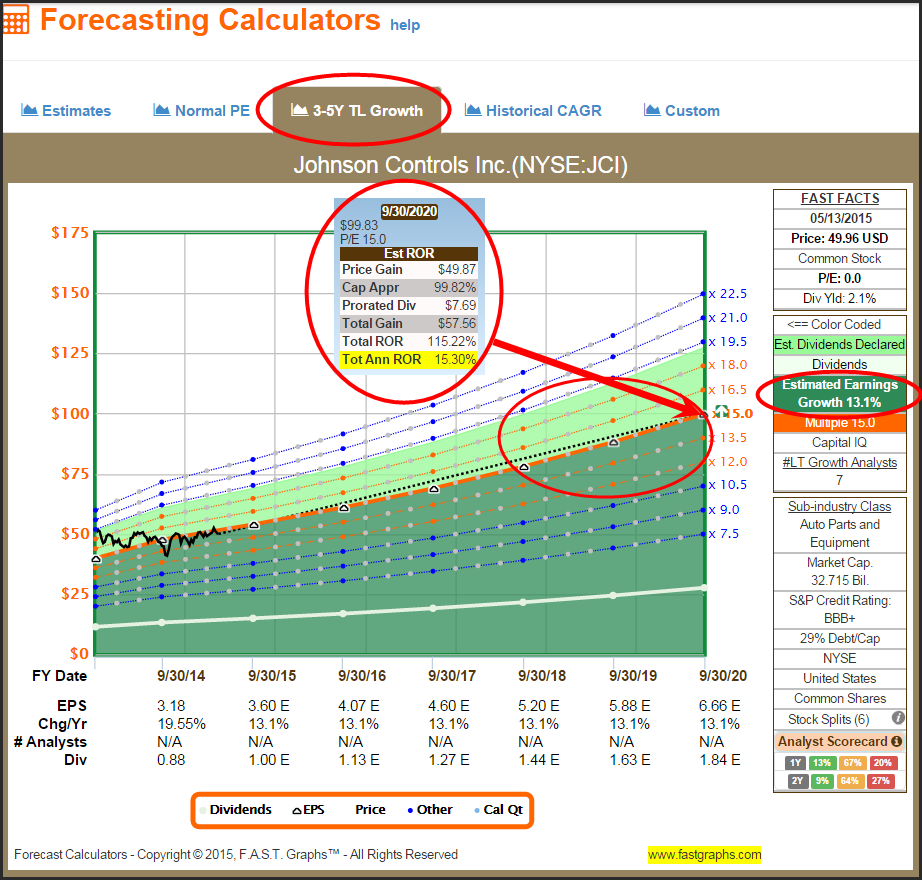

With my final calculation, I will turn to the longer-term 3 to 5 year forecast trend line growth of 13.1% and discover the potential for in excess of 15% annualized total return out to 2020. I also consider this a reasonable estimate considering the transformation that the company has gone through, and the fact that is all but complete. Margins have been improving with the company’s focus on higher margin business, and long-term sales and revenue opportunities are there.

Summary and Conclusions

The stock market as measured by the S&P 500 is, at the least, fully valued and perhaps moderately overvalued. However, that does not simultaneously imply that sound individual investment opportunities are not available. Johnson Controls represents an above-average, long-term total return opportunity that is currently fairly valued in today’s bull market.

Regardless of the level of the overall market, it is rare to find a company that offers double-digit earnings and dividend growth. It is even rarer to find that kind of growth available at a sound valuation. Johnson Controls appears to be a sound total return opportunity that can be purchased at a reasonable blended P/E ratio. Consequently, I believe it is a worthy candidate for a more comprehensive effort.

Disclosure: Long JCI at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

(246)

Report Post